Credit risk analytics software helps financial institutions assess borrower risk using data integration, statistical models, and AI-driven algorithms. Modern lending demands faster, more accurate, and compliant credit decisions, making such systems essential for banks, NBFCs, fintechs, and MFIs. Key features include ETL pipelines, predictive modeling, dashboards, stress testing, regulatory support, and strong data security. Development involves defining objectives, integrating diverse datasets, building ML-based scoring models, creating scalable architecture, and conducting rigorous testing and monitoring. AI further enhances predictive accuracy, real-time scoring, alternative data analysis, and fraud detection. Overall, intelligent credit analytics platforms are shaping the future of digital lending.

Introduction

The skill to forecast/manage the risk of borrowers precisely has turned into a competitive factor in the fast-changing financial world today.

Credit risk analytics software is becoming increasingly popular among banks, NBFCs, and fintech companies to improve decision-making, minimize the number of defaults, and optimize the lending process.

As per the reports, the credit risk rating software market reached USD 10.9 billion in 2023 and is projected to grow at a CAGR of more than 9% from 2024 to 2032. This expansion is fueled by the rising demand for precise credit risk evaluation, reinforced by insights provided by major government authorities.

As the regulatory environments are tightening and customers are becoming more digitally oriented, the need to have a solid credit risk analysis software is no longer an option.

Octal IT Solution is a leading custom software development company offering the best credit risk analytics software with our team of expert professionals.

What is Credit Risk Analytics Software?

Credit risk analytics software is a digital tool that is a specialized program, which gathers, processes, and analyzes the information on a borrower to determine the probability of default.

It uses statistical models, AI algorithms, and real-time data pipelines to arrive at creditworthiness with great efficiency and precision.

Why it matters in modern banking and finance?

Conventional lending was time-consuming, documented less, and subjective. However, nowadays lenders have to make quicker and more consistent judgments and conduct complex portfolios. Bank credit analysis software of modern times assists institutions:

- Improve underwriting accuracy

- Reduce non-performing assets (NPAs)

- Monitor portfolio risk in real time.

- Meet strict regulatory and compliance requirements.

- Enhance customer experience through faster approvals.

With digital lending taking off like a runaway freight train, institutions must have systems that can process huge volumes of data, which are automated to score credit, and those that can incorporate alternative data such as mobile transactions or digital footprints.

It has given rise to a spurt in the demand for sophisticated SAS credit risk analysis solutions, particularly those that run on AI and ML.

What is Credit Risk and Its Importance

What is Credit Risk?

The credit risk is the probability that a borrower will not fulfill his/her financial commitment to the particular obligations, i.e., will not recover a loan or make the necessary payments as agreed upon. It is among the greatest dangers that financial institutions are exposed to.

Types of Credit Risk

| Risk Type | Description |

| Default Risk | Borrower’s inability to repay. |

| Concentration Risk | Excessive exposure to a single borrower, sector, or region. |

| Counterparty Risk | Risk that the other party in a financial contract may default. |

| Sovereign Risk | Risks associated with lending to governments. |

| Settlement Risk | Risk that one party fails to deliver after another party has fulfilled obligations. |

What Is Credit Risk Analytics Software?

Credit risk analytics software is a computer platform that examines borrower risk based on past information, balance sheets, credit agencies, credit profiles, transaction history, and prediction systems. It is meant to streamline and computerize the credit vetting procedure.

Key Functions

A robust system typically includes:

- Data Collection & Integration – Pulls data from internal and external source.

- Credit Scoring Models – Assigns risk scores based on algorithms.

- Portfolio Monitoring – Tracks credit risk exposure across portfolios.

- Risk Modeling – Uses statistical and predictive models for risk calculation.

One of the most popular ways in the industry is credit risk analysis using SAS, and it is beneficial in modeling huge quantities of data and sophisticated scoring models because of the dependability of SAS and its acceptance by regulatory bodies.

Read More: Data Analytics Software Development: Cost & Features

Key Features of a Robust Credit Risk Analytics Software

The project to create effective credit analysis software may involve including several important capabilities:

1. Data Integration and ETL Capabilities

Strong credit analytics entails the combination of data sources with various sources of data, including core banking systems, credit bureaus, financial statements, and digital channels.

ETL pipelines purify and normalize such information and guarantee uniform, high-quality datasets, which are effective and sufficient to model, evaluate risks, and make decisions.

2. Risk Modeling and Predictive Analytics

Predictive statistical models and sophisticated AI/ML algorithms are supported by effective software to forecast the risk of default by borrowers. The credit risk analysis tools, such as logistic regression, decision trees, and random forests, are used to identify historical trends.

Both modern and traditional scorecards offer objective and structured, scalable, and reliable methods of quantifying and comparing credit risk.

3. Dashboard and Visualization Tools

The visualization tools also allow credit teams to quickly interpret the data in interactive forms through a dashboard.

Applications such as Power BI, Tableau, or a bespoke interface may be used to track and follow trends of a portfolio, determine the concentration of risks, and determine the performance of borrowers to make informed and timely decisions based on clear graphical visualizations and real-time analytics.

4. Scenario Analysis and Stress Testing

Scenario analysis software replicates recession, interest rate changes, and industry shocks to determine the strength of a portfolio.

Stress testing reveals the weaknesses and assists the institutions in developing responses to mitigate risks, including readiness to respond to unfavorable situations and enhancing risk management and regulatory capital planning.

5. Compliance and Regulatory Support

To adhere to frameworks such as Basel III and IFRS 9, credit risk systems should allow transparent reporting, audit trails, and regulated model governance.

These capabilities will guarantee proper ECL calculations, regulatory compatibility, less compliance risk, and increased confidence with regulators and stakeholders.

6. Security and Data Governance

Sensitive financial data is secured by strong security measures, including encryption, role-based access, and a secure API.

Good governance guarantees adherence to GDPR and local legislation, prevention of unauthorized access, data integrity, institutional fidelity, safety in operations, and adherence to regulations.

All of these characteristics render the contemporary credit risk analytics software a necessity for financial institutions.

Also Read: Wealth Management Software Development Guide

Step-by-Step: How to Develop Credit Risk Analytics Software

To develop a robust credit risk platform, one needs to plan strategically, employ technical skills, and comply with all regulations. The following is a planned development roadmap:

Define Objectives and Requirements

The definition of the objectives makes sure the credit risk system is aligned with the requirements of the users. Placing the target institutions, like banks, NBFCs, fintechs, and MFIs, assists in the shaping of functionality.

Obvious KPIs include accuracy of the scores, turnaround time, default rates, and efficiency in compliance, which direct design decisions and determine whether the software will meet the expectations of the performance.

Data Collection and Integration

Credit risk assessment cannot be done accurately without high-quality data. The system should incorporate demographic data, bureau data, bank data, statement-parsing data, payment patterns, and other online sources.

An effective ETL pipeline guarantees standard, dependable data that assists in the accuracy of the model and minimizes operational inconsistencies among inputs.

Risk Modeling and Scoring Algorithms

The main component of the system is the risk modeling that relies on logistic regression, decision trees, random forests, gradient boosting, and neural networks.

Fintechs tend to use Python and R instead of SAS, which is used by traditional institutions, but they should calculate PD, LGD, and EAD according to the Basel III and IFRS 9 requirements.

System Architecture and Technology Stack

A good platform must have Python, R, SAS, and SQL/ NoSQL backend processing, a scalable and secure architecture. The UI is driven by React or Angular, and the visualization is also provided by BI tools.

Micro services, APIs, and real-time processing capabilities of analytical works are supported by cloud services on AWS, Azure, or GCP.

Testing and Validation

Reliability is achieved through extensive testing. The validation process on the model is performed through backtesting, sensitivity, and measures such as AUC-ROC, KS, and Gini. Stress tests are tests that consider the performance in unfavourable circumstances.

User Acceptance Testing ensures that workflows satisfy business requirements and perform properly in operational, real-life situations.

Deployment and Monitoring

Implementation is done in phases, and it is integrated with the core banking system, the loan origination system, and the CRM system. Constant supervision identifies model drift, data drift, accuracy degradation, and bias in AI.

To achieve performance stability, compliance, and predictable predictor quality, modern platforms use dashboards to automate performance monitoring across the operation of the system.

How Much Does it Cost to Develop Lending Software?

Lending software development cost is presented in the below table as per their different features.

| Component / Module | Description | Estimated Cost (USD) |

| Loan Origination System (LOS) | Application intake, KYC, underwriting workflow | $15,000 – $40,000 |

| Credit Risk Analytics Module | Scoring models, risk assessment, ML models | $25,000 – $80,000 |

| Loan Management System (LMS) | Repayments, amortization, account management | $20,000 – $60,000 |

| KYC & Identity Verification | OCR, e-KYC APIs, document checks | $5,000 – $25,000 |

| Payment Gateway Integration | UPI, cards, bank transfers | $3,000 – $15,000 |

| Dashboard & Reporting | Portfolio dashboards, BI tools | $8,000 – $30,000 |

| Mobile App (iOS + Android) | Borrower and/or lender app | $20,000 – $70,000 |

| Cloud Infrastructure Setup | AWS, Azure, or GCP deployment | $5,000 – $20,000 |

| AI/ML Automation | Real-time scoring, fraud detection | $20,000 – $100,000 |

| Compliance & Audit Module | Basel/IFRS rules, audit logs | $10,000 – $40,000 |

| Integration With Core Banking/ERP | API development and middleware | $15,000 – $50,000 |

| Total Estimated Cost | Depending on scope and customization | $100,000 – $500,000+ |

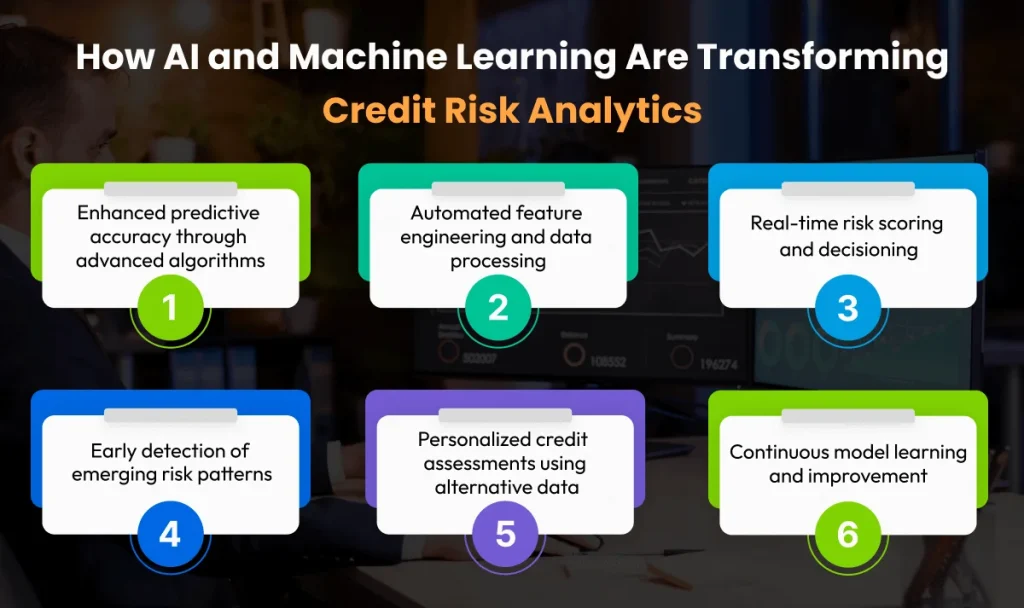

How AI and Machine Learning Are Transforming Credit Risk Analytics

AI and ML are transforming the method of risk assessment by lenders by facilitating more dynamic, granular, and real-time information.

1. Enhanced predictive accuracy using advanced algorithms

Machine learning algorithms can be evolved to a higher level to provide better predictive accuracy, taking into consideration the complex patterns that the traditional models do not capture.

Such methods as gradient boosting, neural networks, and ensemble methods can be used to analyze large amounts of data to make more accurate predictions of default, risk drivers, and more predictive and reliable, data-driven, credit decisions across portfolios.

2. Automated feature engineering, reducing manual effort

Without intense manual effort, automated feature engineering tools detect meaningful variables, transform raw data, and generate optimized features.

This enhances faster model development, minimizes human error, and provides more accurate and predictable predictors, enabling analysts to concentrate on validation, interpretation, and strategic risk decisions.

3. Real-time risk scoring for digital lending apps

Instead of evaluating the applicants over a few minutes, real-time scoring allows the immediate issuance of credit based on the digital lending platforms. Financial, behavioral, and alternative data are processed in real time by the system to assign risk scores to improve the speed of approvals, decrease exposure to default, and increase customer experience in the fast-paced online lending setting.

4. Analyzing alternative data

Alternative data gives more information on the behavior of the borrower, particularly in the case of thin-file or unbanked customers.

Some spending habits, stability, and reliability can be determined by mobile activity, digital payment patterns, and e-commerce histories, allowing lenders to determine creditworthiness more accurately when traditional financial records are limited or unavailable.

5. Continuous model learning, improving performance over time

Continuous learning models automatically upgrade with the incoming data, and thus, they are able to adjust to changes in the behavior of borrowers, market trends, and economic conditions.

This continued optimization makes predictions of credit risks accurate, less prone to drift, and responsive to the real world.

6. Faster detection of fraud and anomalies

Machine learning algorithms detect suspicious patterns, outliers, or deviant behavior of borrowers in a short time, thus preventing fraud.

Quick notifications can be used to avert losses, enhance risk management, and create less-risky portfolios through minimized exposure to fraudulent applications and risky lending practices.

The credit risk analysis software based on AI has become an essential source of competitive edge.

Conclusion

When creating the credit risk analytics software, one needs to have a profound knowledge of financial risk, the latest data technologies, machine learning models, and regulatory frameworks.

With the increase in the extent to which lending is becoming digital and data-driven, banks and fintechs require a system that can analyze large volumes of data, provide risk scores using accurate data, and achieve global standards.

No matter whether you have a big bank providing a sophisticated credit analysis application or a fintech start-up developing AI-based risk scoring, the proper software architecture will enable you to reduce risk, achieve high efficiency, and scale quickly.

Intelligent, automated, and analytics-based lending is the future of the lending industry, and credit risk analytics platforms lie at the heart of this revolution.

FAQs

It is one of the digital solutions that determines the risk of borrowers based on data analysis, statistical models, and machine learning algorithms.

Some of the frequently used tools are Python, R, SQL, SAS, AWS, Azure, and graphical visualization such as Power BI or Tableau.

The AI improves the accuracy of predictions, real-time scoring, and integration of alternative sources of data to assess borrowers better.

It has basic capabilities such as data integration, credit scoring, risk modeling, stress testing, compliance reporting, and dashboards.

By

By June 30, 2026

June 30, 2026