Key Takeaways

- Companies dealing with Blockchain in insurance are growing at a CAGR of 53.09%, and will grow from $2.74 billion in 2025 to $82.56 billion in 2033.

- 5–10% of all claims are bogus, and insurance fraud payments exceed 40 billion dollars per year.

- At a CAGR of 41.05%, smart contracts and parameter insurance currently account for 27.60% of the market revenue.

- Fraud detection is the fastest-growing segment with a CAGR of 57.35%, although claims management leads adoption at a rate of 30.20%.

- 58% of insurance companies are spending more on blockchain, and 77% expect that, within a year, it will be critical to operations, insurance, and claims.

- Blockchain is actively investing through 44% insurance managers, with the US, Europe, and Asia-Pacific leading. Source

- With a CAGR of 54. 72% until 2033, Asia-Pacific is the fastest-growing region.

- Investigation times were reduced using 35% due to facts about Allianz’s blockchain claims center.

Introduction

The insurance industry has long relied on people’s trust that data is stable, claims are paid, and premiums are reasonable. But things appear more chaotic in 2026. Backlogs cause claims to languish for weeks. The industry loses millions of dollars every year due to fraud. Moreover, even easy verification is a manual process due to the siloed statistical structure.

This is where blockchain technology in insurance comes into play, and it is unexpectedly evolving from a catchphrase to a critical part of commercial business operations.

If you’re wondering what blockchain is in the insurance business and why major insurers are rushing to introduce it, the quick fix is

This blog discusses every single factor of blockchain technology in insurance, the path to its potential, the benefits of blockchain in insurance, use cases, implementation methods, local compliance realities, and future developments. This is for you, whether you’re the CTO of a well-known insurance agency, a founder cultivating a brand new blockchain in insurance startups, or an IT executive creating a plan to integrate blockchain and AI into an insurance operation. Now get into it.

Blockchain in Insurance: Market Overview & Growth Statistics

The blockchain in the insurance industry honestly doesn’t expand – it’s taking off.

The international market is expected to grow at a compound annual growth rate (CAGR) of 53.09% to reach $2.74 billion by 2025 and $82.56 billion by 2033 on the strength of fraud losses, automation, and real-time statistical transparency.

The most current market reports you can be aware of are as follows.

| Metric | Data |

| Market Value (2025) | USD 2.74 Billion |

| Projected Market Value (2033) | USD 82.56 Billion |

| CAGR (2026–2033) | 53.09% |

| US Market Value (2025) | USD 0.86 Billion |

| US Projected Value (2033) | USD 25.11 Billion |

| Leading Application | Claims Management (30.20% share) |

| Fastest-Growing Segment | Fraud Detection & Risk Management (57.35% CAGR) |

| Fastest-Growing Region | Asia-Pacific (54.72% CAGR) |

| Annual Insurance Fraud Loss | USD 40 Billion+ |

| Insurers Planning to Increase Blockchain Spend | 58% |

What Is Causing This Expansion?

- The urgent need for format-safe claims data and an increase in fraud losses.

- Development of smart contracts that automate policy execution.

- The growing demand for parametric insurance, especially for the climate crisis and agriculture.

- Real-time statistical reporting is required through guidelines (IFRS 17, Solvency II).

- Insurance companies developing decentralized insurance products are experiencing rapid insurance technology innovation, especially in blockchain.

According to Mordor Intelligence, North America currently holds a market share of 44.30%. However, by 2030, spending in the Asia Pacific is projected to surpass North American spending due to China’s adoption of permissioned chains, FSA regulatory reforms in Japan, and India’s parametric product insurance pilot.

The blockchain in health insurance industry is also becoming familiar. With IBM’s integration with Salesforce in March 2025, more than 500,000 insurance transactions were closed, increasing transparency and eliminating fraud among global fitness insurers.

Data from the insurance sector on the blockchain reveals a clear picture. The message is straightforward: blockchain in the insurance industry sector is now in production rather than testing.

How Blockchain Works in Insurance: Core Concepts and Key Features?

What is Blockchain in Insurance?

In the insurance industry, blockchain refers to a shared virtual ledger that holds the record of all insurance activities, transactions, and claims indefinitely. All legal parties, including insurers, reinsurers, agents, and regulatory authorities, do not see the same cloud data at the same time, as opposed to one insurer keeping all the data in a proprietary database. No one has complete control over it, and no one can subtly alter it.

Core Concepts

- Distributed Ledger

A copy of individual transaction records is stored by each legitimate party within the network. Data silos are eliminated, and real-time cross-party visibility becomes viable as none are owned by a single business enterprise.

- Immutability

A record cannot expire or be changed once it enters the blockchain. Every payment, policy change, and claim submission is permanently recorded with a time stamp.

- Decentralization

There is no factor for failure. Because the statistics are scattered across many nodes, the smartphone is impervious to screws, hacking, and data manipulation.

- Consensus Mechanisms

To prevent fraudulent or unauthorized downloads, a majority of network participants must verify and approve any new files before they are delivered in the chain.

- Cryptographic Security

Cryptographic hashing links each record block to the one before it. Any changes to the program can disrupt the chain and can be significant immediately.

- Public vs. Licensed Networks

Private and permissioned blockchains are becoming most common in the insurance industry, with a market share of 28.50% by 2025. These maintain transparency while only protecting sensitive policyholder records by granting referred contributors the right to access the ledger.

- Tokenization

By tokenizing policyholder data, claims, and risk parameters into enormous virtual representations, secure record sharing is possible without the disclosure of unprocessed personal data. This is particularly relevant for blockchain in health insurance, where sensitive patient data is critical.

Key Features That Make Blockchain Valuable for Insurance

Real-Time Transparency

Disputes between insurers, agents, and reinsurers are reduced because all parties have simultaneous access to the same data.

Automated Audits Trails

Automated logging of all quotes, from policy issuance to payment calls, speeds up and improves the accuracy of compliance reporting.

Interoperability

By connecting disparate insurance and IT infrastructures, blockchain can facilitate communication between modern insurance technology infrastructures and legacy platforms without the need for human interaction.

Zero-knowledge proofs (ZKPs)

A new tool that directly addresses GDPR and HIPAA compliance standards by enabling insurers to verify the accuracy of data (with medical diagnoses) without actually looking at the underlying private record.

The Role of Smart Contracts in Insurance

Most of what makes blockchain applications in insurance honestly useful is powered by smart contracts. They are blockchain-first based automation programs that, once some standards are met, take a move without the need for human approval.

The most straightforward way to approach it:

“If the flight is more than 3 hours behind schedule, as shown with the help of flight information, exchange 200 USD in the policyholder’s wallet.”

No size requirements. There is no name on the adjuster. There is no 3-week delay. It makes it clear.

How Smart Contracts Are Transforming Insurance Operations?

- Automated Claims Processing

Once certain requirements are met, smart contracts immediately start paying after confirming declared conditions for an actual information feed (IoT sensors, weather APIs, clinical databases, police reviews). This frees up the claims backlog, costing insurers thousands of dollars in overhead every year.

- Policy Insurance & Management

The smart contract directly incorporates policy terms. There is no paperwork or manual processing involved; insurance starts as soon as a premium payment is verified on the blockchain.

- Parametric Insurance

Smart contracts are maximally useful in this example. Measurable events where storms reach certain wind speeds, rainfall falls below the threshold, or crop yields fall below the baseline trigger payouts in parametric (index-based after all) insurance. These payouts are processed automatically with the help of smart contracts that are linked to reliable information about the data.

- Fraud prevention

Without exception, smart contracts practice uniform business guidelines for each declaration. They should regularly catch irregularities or false filings through pass-reference claims with insurer entries in the general ledger.

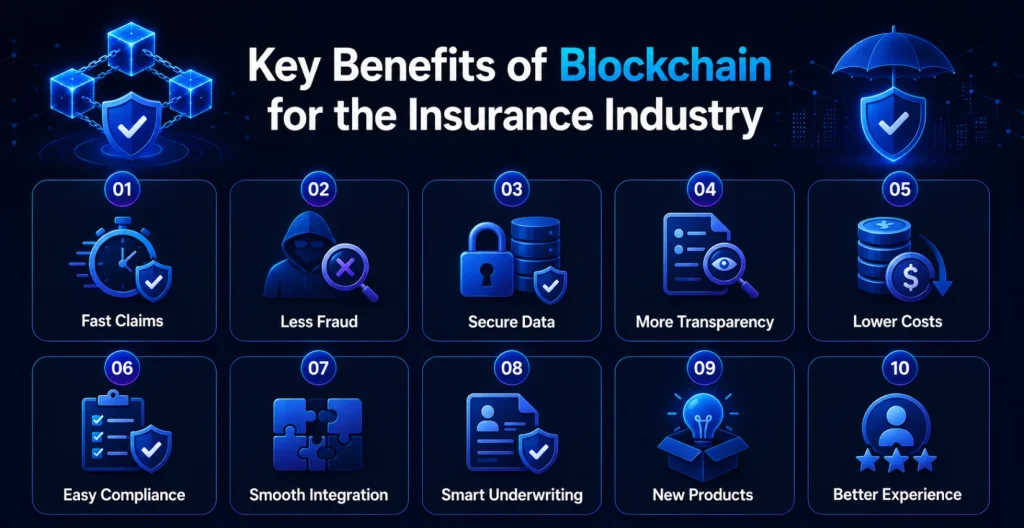

Key Benefits of Blockchain for the Insurance Industry

The following explains blockchain uses in insurance by insurers around the world and why it makes for the best business experience:

Fast Claims Processing

By offering everyone access to a shared, real-time ledger, blockchain removes the need for manual verification techniques. Once the claims are satisfied, smart contracts automate the agreement, cutting the time in claims processing from days to weeks or hours or minutes. Because of Allianz’s multi-country blockchain hub, the usage of 35% reduced the duration of the search cycle.

Drastically Reduced Fraud

It is almost impossible to verify more than one claim, create an identity, modify historical records with unchanged facts, or transfer-side visibility. Industry estimates suggest that blockchain-enabled fraud detection systems should reduce fraud claims by up to 75%.

Enhance Data Security

Compared to centralized databases, insurer statistics, and cryptographic hashing, decentralized storage is mostly a steady path. This is especially important regarding blockchain in health insurance because clinical records are sensitive.

Increased Trust & Transparency

With the help of all stakeholders, including brokers, insurers, reinsurers, and regulators, the same irrefutable facts are visible. Often, the “he said, she said” arguments that delay the inducement deal and raise labor charges are dismissed as a result.

Lower Operating Costs

Reliance on manual processing is decreased by automating underwriting, policy administration, and claims. According to McKinsey, blockchain could save reinsurers alone up to $10 billion in yearly operating expenses.

Improved Regulatory Compliance

Time-stamped records and irreversible audit trails improve the effectiveness and reliability of compliance reporting. Using smart contracts, rules can be enforced mechanically, ensuring uniform compliance for all transactions.

Smooth Reinsurance & Trade Finance Integration

Blockchain has a significant impact on changing finance and debt insurance. The common ledger allows all parties to collaborate on contingency transfers, interest, and claims in real time, reducing the reconciliation disputes and settlement delays that previously plagued cross-border reinsurance.

Improved Underwriting Accuracy

The role of blockchain in trade finance and credit insurance is significant. Blockchain enables more accurate pricing and threat assessment by providing insurers with proven, real-time, tamper-proof records from clinical structures, IoT equipment, and third-party resources.

New Insurance Products

Peer-to-peer insurance models, parametric policies, crypto/digital asset insurance, and on-chain ESG-linked systems are all made viable by blockchain and cannot be improved with legacy infrastructure.

Improved Customer Experience

Automated interactions, transparent policy tracking, and quicker payouts all increase consumer trust and lower the friction that causes policyholder attrition.

Real World Use Cases of Blockchain In Insurance

Exploring what just works within the real world is a great technique to learn how blockchain technology can be used in insurance. These blockchain use cases in insurance include digital assets, crops, health, marine, and reinsurance:

Claims Processing Automation (Allianz)

Allianz has eliminated manual reconciliations between nearby workplaces and reinsurers with the help of the use of a multi-country blockchain claim center, which reduces instances of discovery cycles by using 35%.

Marine & Cargo Insurance

Insurewave, based on the Korda blockchain, connects AP Moller and Maersk insurance contracts with real-time shipping information. It enables dynamic, uniform pricing and reduces paperwork between vendors, including XL Catlin, MS Amlin, and Willis Towers Watson, by presenting real-time visibility into property areas, conditions, and security.

Parametric Flight Insurance

When flights are not punctual beyond a certain amount, smart contracts covering air traffic facts trigger mechanical refunds without ever filing a declaration from the buyer.

Health Data Exchange

The blockchain-powered network, supported by Avaneer Health, Aetna, Anthem, and the Cleveland Clinic, addresses key issues with blockchain in health insurance by updating claims processing, ensuring the flow of health records, and the accuracy of certain provider records.

KYC & Identity Verification

Blockchain-department KYC (Know Your Customer) networks save fees for insurers and stop customer onboarding problems by allowing multiple insurers to safely exchange the effects of identity verification.

Reinsurance Settlement

Blockchain-based reinsurance ledgers that enable real-time record sharing between insurers and reinsurers and eliminate reconciliation delays and contract disputes were tested using the B3i consortium, including Achmea and 15 different insurers.

Peer-To-Peer Insurance

Etherisc is powering decentralized insurance products, including deferred crop, hurricane, and aviation cover, where policyholders form pooled combination schemes managed through smart contracts without the need for a traditional insurance carrier.

Credit Insurance & Trade Finance

Blockchain significantly reduces the threat of fraud and accelerates credit score selection at all levels of worldwide chains of delivery with the help of enabling real-time verification of change documents, invoices, and payment histories in the credit insurance company. This is one of the most profitable blockchain applications in insurance solutions.

Digital Asset Insurance

Blockchain provides a native infrastructure to secure, monitor, and validate the rules of virtual assets, a market category that became non-existent 5 years ago as the use of cryptocurrencies and Web3 increases.

Blockchain in Insurance: Cost, ROI & Business Case

“What is this cost, and what do I really get?” This is the first question every insurance manager asks. Here is an honest answer.

Estimated Implementation Cost

| Implementation Component | Estimated Cost Range |

| Blockchain Strategy & Architecture Consulting | USD 20,000 – USD 80,000 |

| Smart Contract Development & Auditing | USD 30,000 – USD 150,000 |

| Platform Integration (Hyperledger, Ethereum, R3 Corda) | USD 50,000 – USD 250,000 |

| Legacy System Integration & APIs | USD 40,000 – USD 200,000 |

| UI/UX & Insurance App Development | USD 25,000 – USD 100,000 |

| Security Audits & Compliance Setup | USD 15,000 – USD 75,000 |

| Staff Training & Change Management | USD 10,000 – USD 50,000 |

| Ongoing Maintenance & Node Infrastructure | USD 20,000 – USD 80,000/year |

| Total MVP Estimate | USD 100,000 – USD 500,000 |

| Enterprise-Scale Full Deployment | USD 500,000 – USD 2,000,000+ |

Note: The size of the business, the scope, the platform, and the difficulty of integrating existing systems all have a significant impact on the cost. Custom quotes can be provided with the help of an experienced insurance app development company.

ROI Drivers

- Fraud Reduction

Even a 20% reduction in fraud can allow a medium-sized insurance company to collect tens of thousands and thousands of dollars annually, given that 5–10% of all claims are fraudulent and international losses top 40 billion dollars annually.

- Claims Processing Efficiency

By eliminating guide estimation, paper handling, and adjuster overhead, claims intelligent reconciliation automation can reduce processing fees in line with the 30 to 50% statement.

- Reinsurance Cost Savings

According to McKinsey, blockchain could additionally eliminate reconciliation delays and disputes, saving the reinsurance company up to $10 billion per year.

- Reduced Administrative Overhead

According to DXC Technology and ServiceNow, computerized insurance systems can reduce operational costs associated with manual processing by up to 40%.

- Customer Retention

Declaring settlements faster and free insurance management reduces churn directly. Long-term revenue can improve dramatically with even a 5% increase in retention.

The Business Case in One Line

Before considering performance updates, new product sales, and competitive differentiation, the majority of medium to large insurers position that the use of blockchain technology can honestly pay for itself in 12 to 24 months through fraud savings.

How to Integrate Blockchain in Insurance Operations: A Step-By-Step Process

From the initial method to the actual deployment, this is a useful roadmap for implementing AI and blockchain in insurance operations.

1. Define Your Use Case & Business Objectives

Determine exactly what problem you’re addressing – claims fraud, term settlement, reinsurance reconciliation, or KYC duplication – before using any technology. A smart “let’s put everything on the blockchain” mandate threatens much less technology than a focused use case. Immediately contact your IT and operations departments.

2. Conduct a Technology and Infrastructure Audit

Examine current statistical management frameworks, policy management systems, claims databases, legacy masterworks, and systems. Determine which areas the blockchain will replace, where it will connect, and what intermediaries or APIs may be needed to connect the new and legacy infrastructure.

3. Choose the Right Blockchain Platform

Select the platform that best suits your use case and compliance needs. The most used option for enterprise insurance is Hyperledger Fabric (non-public, GDPR-happy, permissive). R3 Korda is quite good at financial settlement and reinsurance. Ethereum is a good choice for parametric or decentralized hedging products. This choice should be based on your particular architecture and the insurance software developer you have selected.

4. Design Smart Contracts & Data Models

Create a smart contract that we primarily base on your business rules, insurance eligibility, claim trigger, fraud assessment and payment status. Blockchain creators and professionals in the field of insurance should draw closely from this section. Independently test each smart solution for security flaws before implementation.

5. Build & Integrate

Create frontend user interfaces, APIs, and integrations for your insurance CRM software program. To ensure that users (integrators, vendors, and customers) have smooth access to the blockchain-powered workflow, the environment in which your insurance comparison mobile app development is built. Use the blockchain app development services of supportive allies to accelerate this step.

6. Test in a Controlled Environment

Use a small number of regulations, claims, or reinsurance contracts for proof of concept (PoC) or testing. Use real records whenever possible. Evaluate overall performance against your baseline KPIs, fraud value, settlement value, deal accuracy, and claims cycle time.

7. Compliance & Regulatory Sign-Off

Verify that you manage all relevant requirements (including Solvency II, GDPR, IRDAI, HIPAA, and U.S. Insurance Law with the State) before scaling up. Involve your legal team, and actively consult with regulators as needed. For regulatory assessment, report your data governance version, audit trail processes, and smart contract good judgment.

8. Full Deployment, Training & Monitoring

Start producing at maximum capacity. Teach new workflows to your insurance, claims, and operations teams. Create non-stop tracking dashboards to maintain tabs on claims cycle times, fraud-flag accuracy, smart contract executions, and blockchain node security. Continuously optimize with real-time facts.

Common Challenges of Integrating Blockchain & How to Overcome Them

Challenge 1: Legacy System Incompatibility

The majority of insurers are using outdated technology that was never meant to talk to the blockchain community.

Fix: To connect old to new, use an API layer known as middleware. Instead of totally rebuilding everything without delay, start with a module like the claims. An official insurance app development agency will take care of this without interfering with the actual operation.

Challenge 2: Scalability Limitations

When claims pile up without delay, the public blockchain can also slow down quickly.

Fix: Choose a permissioned blockchain designed for large chunks, including Hyperledger Fabric or R3 Corda. It is for this reason that hybrid architectures are growing at a CAGR of 56.40%: they offer internal speed and external audit capabilities.

Challenge 3: Data Privacy & GDPR Compliance

People have the right to be forgotten, in line with the GDPR, but blockchain does not. It’s an extreme battle.

Fix: Keep personal information off the chain. Only the cryptographic hash should be stored in the ledger. Validate claims using 0-knowledge proof (ZKP) without ever disclosing the underlying data. This strategy is already supported by the EU government.

Challenge 4: Industry-Wide Adoption & Consortium Building

Blockchain is at its simplest and most effective when all participants are connected to a community. It’s hard to get rivals to agree on anything.

Fix: Don’t start from scratch when growing a network. Join already existing alliances, together with B3i or RiskStream Collaborative, where sponsors are already on board, and standards are already in place.

Challenge 5: Smart Contract Vulnerabilities

Incorrect payments can also be the result of malicious activity in a smart contract, and this cannot be reversed on the blockchain.

Fix: Before the smart contract goes live, audit it independently. Include operating systems and use testing frameworks like OpenZeppelin to allow authorized parties to perceive and deal with problems.

Challenge 6: Talent Shortage

It is quite hard to find engineers who are knowledgeable about almost every blockchain and insurance.

Fix: Instead of starting from scratch, partner with a specialized company. Additionally, you can collaborate with teams that offer blockchain shipping along with iOS and Android app development, or hire insurance software developers with verified blockchain portfolios.

Regulatory & Compliance Considerations by Region

One thing with blockchain in insurance industry that gets forgotten occasionally is the reality that neighborhood laws are considerably pervasive. In Europe, surveillance in the United States is forced or unpaid. But British regulators may be wondering what India is supporting. Blockchain can conquer those differences instead of exploding them.

Here are some examples where blockchain applications in insurance are aligned with the necessary regulatory framework and where they truly help in choosing the creation of new issues.

1. USA (🇺🇸)

Since insurance is governed by state regulations, each state has specific rules for eligibility, creditworthiness, and damages. The GENIUS Act (2025) provides the leading government stablecoin framework relevant to parametric payments, and HIPAA governs on-chain health information. Blockchain includes nationally precise rules in smart contracts and automates forensic investigations; However, if these guidelines are written incorrectly, the error will automatically spread to all candidates.

2. European Union (🇪🇺)

The immutability of the blockchain and the “right to be forgotten” of the GDPR are in direct competition. The answer is to use ZKP for verification, trading for the simplest hashes, and keeping personal information off-chain. Although only 15% of EU insurers now use blockchain, it is far from in line with the Solvency II report (EIOPA, 2024). Fines for GDPR violations can reach up to 4% of an arena’s annual revenue.

3. India (🇮🇳)

Blockchain-first-based claims transfers are actively supported through frameworks such as ABDM and HCX, and IRDAI oversees the market. Built payment delays are already decreasing from weeks to days for weather oracle smart contracts. Warning: In an area where the insurance penetration rate is about 3.8%, automated eligibility exclusions without human control could solidify access gaps.

4. US (🇬🇧) & Asia Pacific

While Lloyds investigates chain syndicate fact-sharing and the UK’s FCA sandbox allows blockchain trials, it is far from clear whether the smart contracts are legally enforceable under English law. In the Asia-Pacific region, Singapore’s MAS has established a clear law for cryptocurrency-related hedging products, China is assisting with permissioned blockchain, and Japan’s FSA is transitioning to ledger-friendly solvency measures by 2026.

Bottom Line: Local law guidelines have not been replaced through blockchain. When well designed, it speeds up and improves auditability. Carelessly constructed, non-compliance is scaled at machine speed.

Future Trends of Blockchain in the Insurance Industry

AI + Blockchain Convergence

With the help of AI trained on blockchain-verified claims records, fraud is detected in hours, not weeks. The development of a legitimate plan to integrate blockchain and AI into insurance operations quickly evolved into a pressing need to “stand out.”

Tokenization of Insurance-Linked Securities

With on-chain tokenization of reinsurance contracts and default mortgages, a new magnitude of capital market traders is attracted. By 2031, this market category is estimated to grow to approximately US$1.7 billion (Mordor Intelligence).

Digital Asset & Crypto Insurance

Coverage of smart housing uses, hot wallets, and swaps is widely called out. In early 2025, the BDIC deliberately selected Bermuda as its global headquarters for underwriting digital wallet risks, a category that essentially became non-existent three years ago. To construct it properly, insurers joining this market require expert blockchain app development services.

Zero-Knowledge Proof Integarton

Regardless of the facts of the patient, ZKPs allow insurers to verify the declaration, along with verifying that the diagnosis meets the coverage requirements. This solves the GDPR/immutability hassle, preventing the implementation of blockchain in European health insurance.

Decentralized Insurance & DeFi Models

Without a traditional insurer in the middle, platforms like Etherisc allow insurers to vote on claims, pool threats, and access automated reimbursement in niche markets that are still in their infancy but are still growing rapidly.

Parametric Insurance at Scale

Automatic reimbursements for droughts, wildfires, and floods are becoming a reality thanks to blockchain-connected IoT sensors and satellite feeds; no claim form is required. Teams that hire mobile app developers with IoT integration knowledge are best positioned to construct this blockchain, which is the fastest-growing blockchain in insurance use casesworldwide.

On-Chain ESG & Sustainability Reporting

Especially in Europe, where regulatory calls for ESG transparency are highest, insurance companies are using blockchain to create verifiable, tamper-proof audit trails for ESG-related products. This is an expanding blockchain in insurance market opportunity.

Cross-Border Insurance Networks

By 2027, the G20’s digital economic transaction framework will enable real-time sharing of the history of KYC claims, making a multi-jurisdictional insurance network blockchain economically viable.

Implementing Blockchain in Insurance With Octal IT Solution

The right technology is important, but so is the right IT partner. At Octal IT Solution, we help you get from strategy to live implementation without the typical delays, cost overruns, or compliance issues by fusing our extensive insurance domain knowledge with tried-and-true blockchain engineering.

1. End-To-End Blockchain Expertise

We deal with the entire lifecycle from architecturally smart contract solutions to full-stack blockchain app development services, saving you the hassle of managing many companies.

2. Custom Smart Contract Development & Auditing

For claims automation, policy management, fraud detection, and parametric payments, we configure, build, and independently audit smart contracts to ensure they are secure, legal, and impervious to exploitation before going live.

3. Insurance Domain Specialization

We are an experienced insurance app development company with considerable expertise in regulatory rules, coverage workflows, and gadget integration problems. Building software applications and building insurance applications are different, and we know this.

4. Legacy System Integration

Our teams are experts at bridging the old and the new, using custom API middleware to connect your modern databases and policy management systems to the blockchain network without interfering with ongoing business strategies.

5. Medical Claim Processing System Development

Our blockchain-based absolute medical advertising treatment device improvement solution reduces leading touchpoints, automates verification, and adheres to neighborhood and HIPAA fitness fact standards.

6. Full Stack Mobile & App Development

Using blockchain-powered Android and iOS app development, we build insurance assessment mobile application development, responses, defender-going through portals, and agent dashboards.

7. Insurance CRM Software Development

When you get our Insurance CRM app development, your revenue, insurance, and claims teams will have a verifiable, real-time view of every policyholder’s interaction path for our integration of blockchain fact layers into CRM systems.

8. AI + Blockchain Roadmap Consulting

We help you develop and execute a workable plan for integrating blockchain and fact infrastructure with AI in insurance analytics for fraud detection, threat assessment, and claim prediction.

9. Data Analytics in Insurance Industry

Your blockchain facts are transformed into usable intelligence through our analytics layer, which performs known fraud patterns, claims development, enhances company selection, and signature verification.

10. Regulatory Compliance Built In

To protect you from the start, we layer each blockchain solution with regional compliance, GDPR, HIPAA, IRDAI, and state-individual US coverage requirements, among others.

11. Dedicated Talent On Demand

Need to scale quickly? Take advantage of our pre-tested team to create insurance applications, hire iOS app developers, or hire Android app developers who are already downloaded and included in your project from the start, with an insurance domain reference.

12. Health Insurance Software Development

We offer mobile app development for health insurance that use blockchain technology for record-breaking security, interoperability, and fraud prevention, from virtual health playing cards to automated decision notifications.

Wrapping It Up

Insurance blockchain already works – not just theoretically, but closely anyway. We talked about how it speeds up claims, reduces fraud, uses smart contracts to automate signatures, enables parametric payments, and satisfies regulatory standards in the US, EU, India, and other countries.

By 2033, the market is expected to grow from $2.74 billion to $82.56 billion. Every year, fraud costs 40 billion dollars. The actual regulations are processed through smart contracts. Within two years, 77% of insurers expect blockchain to be essential to their business, and the use cases and ROI have been proven.

Time is the only real question, and the longer you wait, the more difficult it is to catch up.

By

By June 26, 2026

June 26, 2026