Insurers that are data-driven apply analytics to reduce fraud, pricing, personalise products, and simplify claims. Investment in insurance analytics is booming very fast in the market because of the growth in data and regulation.

- Introduction

- What is Data Analytics in Insurance?

- Why Data Analytics Matters: The Importance of Data Analytics in Insurance

- What is the Role of Data Analytics in Insurance?

- How is Data Analytics Used in Insurance – Practical Applications

- Data Analytics in Insurance Examples (Concrete Use Cases)

- Benefits of Data Analytics in Insurance

- Impact of Data Analytics in Insurance

- Challenges of Data Analytics in Insurance

- Technical & Organizational Best Practices (How to succeed)

- Future of Data Analytics in Insurance

- Case Study Spotlight: Two Success Stories

- Implementation Roadmap- From Pilot to Scale

- Conclusion

- FAQs

Introduction

The insurance industry is in a seismic rise. As the choice was previously shaped by actuarial tables and archaic systems, it is now being transformed by real-time insights, machine learning frameworks, and connected device telemetry. Insurance Data Analytics is not a single pilot project any longer: it is a fundamental strategy. The structured and unstructured data are used to maximise pricing, detect fraud, automate claims, improve customer experience, and open new product lines, which is done by insurers. This is changing, and can be summarised as Data analytics in insurance industry adoption, which is designed to enable the carriers to reduce costs, enhance risk management, and compete against digital-first entrants.

Here, we discuss the definition of data analytics in insurance, its practical use, advantages, and impact, real-life examples, issues, and the direction the technology is taking.

What is Data Analytics in Insurance?

Data analytics in insurance is the methods, tools, and processes that an insurer employs in gathering, processing, and analyzing data to extract actionable information that can be used in underwriting, claims, distribution, pricing, customer retention, and compliance. It spans:

- Descriptive analytics (what has happened): Premiums, loss ratios, claims frequency, dashboards, and reporting.

- Diagnostic analytics (why it happened): Spike in claims or unexpected reserve changes, root causes.

- Predictive analytics (what is likely to occur): Models that predict the likelihood of a claim, customer churn, or future premium volume.

- Prescriptive analytics (what to do): Using machine learning and optimization algorithms to optimize pricing, channel mix, or routing of claims.

Some data sources include policy systems, claims databases, telematics and IoT devices, social media, third-party data (credit, weather, property records), geospatial data, images, and voice transcripts. The combination of these helps the modern insurer to make quicker and more accurate decisions.

| Latest market snapshot: The global insurance analytics market was valued at USD 14.50 billion in 2024. The market is projected to grow from USD 16.70 billion in 2025 and reach USD 43.95 billion by 2032, exhibiting a CAGR of 14.8% during the forecast period. |

Why Data Analytics Matters: The Importance of Data Analytics in Insurance

The importance of data analytics to Insurance is explained by the fact that it could transform the information into a competitive advantage:

- Risk differentiation and proper pricing: Granular models can also be used to price to individual risk rather than cohort averages.

- Elimination of fraud: Fraud is detected faster through network analysis and anomaly detection.

- Operation efficiency: Routine operations are automated, reducing processing costs and cycles.

- Excellence in customer experience: Personalised offers and faster settlement of claims improve retention and NPS.

- Regulatory compliance and reporting: Correct and auditable solvency and regulatory reporting can be generated with the help of analytics.

- New product innovation: The analytics show the unmet needs that would permit the parametric products, usage-based insurance (UBI), and micro-insurance.

Incorporating analytics into decision processes can be applied to reduce combined ratios, lower leakage, and increase the lifetime value of a customer, and therefore, analytics is a strategic need rather than a back-office toy.

What is the Role of Data Analytics in Insurance?

The main position of analytics is to be the decision engine in the insurance value chain:

- Underwriting: Predictive score of risk, automatic document extract (NLP), and external data enrichment accelerate risk decisions and keep risk manageable.

- Pricing: The models of dynamic and real-time pricing will be based on individual and external behavior (e.g., telematics) and the external conditions (weather, economic indicators).

- Claims: Triage automation, analyzing images/video to determine the level of damage, and detecting fraud decreases settlement time and enhances accuracy.

- Customer acquisition and retention: Propensity models are used to identify potential buyers and forecast renewal/non-renewal risk; next-best-action systems are used to determine cross-sells.

- Capital & reserves: Reserve adequacy and capital planning are supported by stress tests and stochastic modelling.

- Operational analytics: Workforce optimisation, process mining, and KPI dashboards cut the bottlenecks and manual rework.

Just as financial institutions increasingly integrate AI ML with banking to enhance fraud detection, personalization, and predictive insights, insurers are adopting similar AI-driven frameworks to strengthen underwriting precision, pricing models, and risk management. This convergence showcases how advanced analytics can transform traditional processes into intelligent, outcome-based ecosystems.

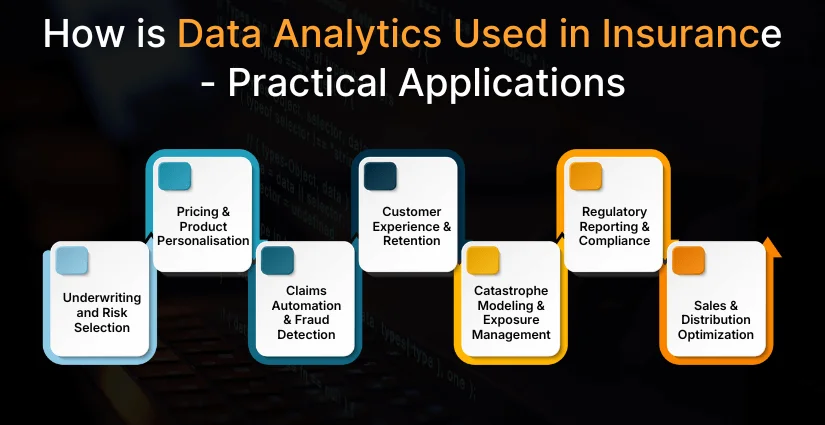

How is Data Analytics Used in Insurance – Practical Applications

The following are practical industry-tested applications of how data analytics in insurance industry can transform data into quantifiable results:

Underwriting and Risk Selection

- Machine learning frameworks consume historical loss data, telematics data, property features, and third-party cues to score applicants.

- Automated data enhancement (property pictures, claims history) minimizes manual underwriter examination.

Pricing & Product Personalisation

- Telematics is applied in usage-based insurance (UBI), where safer drivers are charged less.

- Behavioral pricing is one that packages premiums and discounts according to customer segments.

Claims Automation & Fraud Detection

- Computer vision analyzes vehicle/property damage based on photographs; NLP detects facts on claims forms.

- Networks’ Anomaly detection and graph analytics identify suspicious patterns of claims.

Customer Experience & Retention

- Propensity models anticipate the lapse risk and initiate individualised retention deals.

- Chatbots and virtual assistants pass the contextual response and case escalation through analytics.

Catastrophe Modeling & Exposure Management

- Typically, real-time feeds (weather, insurer exposure maps) allow the simulation of scenarios and rebalance the portfolio before the losses are incurred.

Regulatory Reporting & Compliance

- Analytics automates solvency, anti-money-laundering checks, and regulatory filings report generation to enhance timeliness and accuracy.

Sales & Distribution Optimization

- Channel analytics provides details on which brokers or digital channels generate profitable customers; marketing spend is optimised by ROI models.

Data Analytics in Insurance Examples (Concrete Use Cases)

Data analytics software development empowers insurers to leverage real-time insights for smarter decisions. It enhances fraud detection, claims automation, customer personalization, and predictive underwriting, driving efficiency, accuracy, and profitability across insurance operations.

Auto Insurance Telematics:

This is a technique that insurers use to collect driving behaviour by installing devices in cars or using smartphone apps to reward safe drivers with reduced premiums. It helps insurers personalize policies, improve risk assessment, and encourage safer driving habits among policyholders.

Settlement of Claims Based on Images:

Insurers that automatically determine the value of vehicle damage based on uploaded photos reduce the average claim settlement time from days to hours. This not only speeds up payouts but also enhances customer satisfaction through quick, hassle-free service.

Fraud Ring:

Based on social network analysis and common data, companies detect organized crime rings and pay less. By uncovering hidden connections between fraudulent claims, insurers can significantly reduce financial losses.

Crop/weather Event Parametric Insurance:

Satellite and weather data automatically pay out on attaining set thresholds. It ensures farmers receive instant compensation without lengthy claim verification processes.

Predictive Churn Models:

Model predictions can be used to run focused retention campaigns that lower churn by a few percentage points, which increases lifetime value. By identifying at-risk customers early, insurers can take proactive steps to improve engagement and loyalty.

Also Read: Data Analytics in Finance: Key Use Cases and Benefits

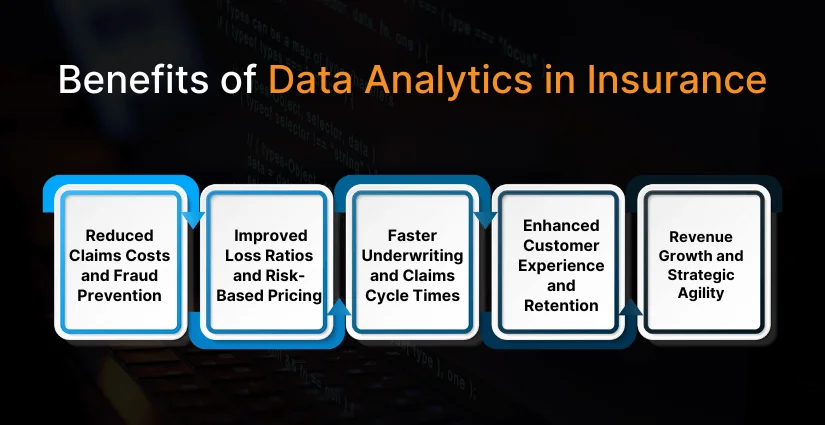

Benefits of Data Analytics in Insurance

The advantages of data analytics in insurance are much more than the improvement of operations, remodeling underwriting, pricing, claims, customer experience, and long-term business strategy. The following is a breakdown of the main benefits that insurers stand to acquire when using analytics in their core operations.

1. Reduced Claims Costs and Fraud Prevention

A major reduction in costs of claim is one of the short-term advantages of the continued impact of reduced costs. The traditional claims have affected the insurer’s profitability due to fraud claims, leakage claims, and manual processing errors. Analytics will help insurers identify suspicious trends at an early stage, automate the process of claims triage, and put the cases with high risks at the top of the investigation list. Machine learning programs evaluate the historical claims, repair estimation, customer behavior, and third-party data to indicate irregularities to minimize risks of fraudulent payment. There is also less reliance on manual review, which reduces the administrative overhead and ensures faster settlements without reducing the accuracy.

2. Improved Loss Ratios and Risk-Based Pricing

What data analytics provides is accuracy in risk evaluation and pricing, which directly increases the loss ratios. The classical actuarial models were based on the general categorisation of the customers, whereas modern analytics are able to employ telematics, behaviour analysis, and IoT devices data, as well as historic claims to determine the risk on an individual basis. Better pricing eliminates adverse selection and instills the right premium based on actual risk exposure. This assists insurers in staying profitable as well as providing more reasonable prices to the customers.

3. Faster Underwriting and Claims Cycle Times

Insurers have enjoyed reduced turnaround times in all core processes through straight-through processing, automated risk profiling, and AI-driven decision engines. Approval of underwriting, which used to take days to be completed, takes minutes, and claims, which used to take a long time to be evaluated manually, can be done almost instantly using automated tools. Shortened cycle time improves internal efficiency, minimizes operational delays, and gives the employees time to work on complex and high-value cases.

4. Enhanced Customer Experience and Retention

Analytics will assist insurers in providing one-on-one and smooth customer experiences. Insurers can optimise product suggestions, proactively assist, personalize costs, and send alerts or renewal offers on time with predictive insights. Service quality is also improved with the help of AI-driven chatbots and sentiment analysis. Finally, increased customer satisfaction and loyalty, higher Net Promoter Scores (NP) are the result of faster settlements, personalised policies, and better digital interactions.

5. Revenue Growth and Strategic Agility

Through customer behaviour, customer life events, and purchase intentions analysis, the insurers can help unlock new revenue sources by offering targeted cross-sell and upsell offers. Strategic agility is also enhanced by analytics, as it makes it possible to monitor in real-time, predict, and plan a scenario. Faster response to market changes, emerging risks, and competitive pressure will enhance long-term growth and resilience as insurers are able to react quickly to them.

Impact of Data Analytics in Insurance

Data analytics effects in Insurance can be summarized into the following: operational, financial, and strategic results:

- Operational: Reduced rate of manual errors, automated workflows, and staff optimization.

- Financial: Better combined ratio, less money paid in fraud, and increased retention-based revenue.

- Strategic: Product innovation (parametric, on-demand), partnerships (insurtech integrations), and data-driven distribution strategies.

At the macro level, market spending on analytics reflects insurers’ perception that information is one of the most vital assets for securing market share and opening new revenue streams.

Challenges of Data Analytics in Insurance

And despite the positive aspect, there are actual challenges when it comes to the implementation of data analytics in Insurance:

- Information quality and information integration: Old policy/claims systems, data silos, and discrepant identifiers make it difficult to see a unified picture.

- Privacy & regulation: Sensitive personal data, international data transfers, and new regulations (GDPR, local regulations) need to be handled with care.

- Model governance & explainability: Black-box models can be an issue because insurers have to validate them and explain them to regulators and business users.

- Talent and culture: To enable analytics, the data scientists, MLOps, and change management have to shift the decisions into data-driven workflows.

- Operationalising models: Models have to be productionised, monitored, and retrained for a large number of pilots to break at scale.

- Prejudice and equality: Biased data may lead to unfair prices or discounts; companies need to identify and overcome prejudgment.

- Cost & old technology debt: It may be costly and time-consuming to substitute or unify old systems.

To overcome these difficulties, it is necessary to follow a practical roadmap: focus on high-value use cases, invest in data hygiene, introduce model governance, and create cross-functional teams.

Read More: Data Analytics in Healthcare: Key Use Cases & Benefits

Technical & Organizational Best Practices (How to succeed)

In order to optimise ROI on Data Analytics in Insurance, insurance companies should consider the following best practices:

- Begin with the business value: Identify use cases that can be quantified in terms of KPIs (fraud reduction, claim cycle time).

- Create a modular data platform: Cloud data lake + governed data marts + models feature store.

- Invest in MLOps and automation: CI/CD of models, data drift monitoring, and retraining (autonomously).

- Powerful data controls: Lineage, access controls, privacy-by-design.

- Explainable models: Explainable models are preferable when the regulatory scrutiny is intense; SHAP/LIME explanations should be employed when necessary.

- Cross-functional teams: Two underwriters and claims professionals with data scientists to reduce the iteration time.

- Find a partner: Take advantage of insurtechs to have certain functions (telematics, parametrics, image analysis) instead of doing everything in-house.

Future of Data Analytics in Insurance

The future of data analytics in insurance is evolving with deeper AI and edge integration. With generative AI development services, insurers can enable real-time underwriting, automate document processing, and personalize customer engagement. Edge and IoT analytics will let devices like cars and industrial sensors process localized data for dynamic risk assessment.

Federated learning will ensure privacy-preserving model training, while parametric and usage-based insurance models will automate claims through trusted IoT or satellite indicators. Additionally, embedded insurance will use analytics to tailor micro-products within digital ecosystems, reshaping product design, risk transfer, and customer relationships in the insurance industry.

Case Study Spotlight: Two Success Stories

Use case A – Claims automation with computer vision & fraud scoring

- Problem: The cost of high manual inspection and settlements that are not consistent.

- Data inputs: Claimant photos, past claims, repair shop records, vehicle telematics, social signals.

- Analytics stack: Image pre-processing → CNN model to estimate repair cost → fraud-score model using gradient boosting → rules engine for auto-approval thresholds.

- Outcome: Auto-settlement for low-cost, low-risk claims; faster payment, reduced adjuster load, and a measurable drop in average claim cycle time.

Use case B -Telematics & personalised pricing for auto insurance

- Problem: When we price using coarse surrogates, we end up with adverse selection.

- Data inputs: Driving behavior, frequency of trip, geolocation risk, and time-of-day driving.

- Analytics stack: Feature engineering for behavior scores → survival models for claim probability → real-time scoring and mobile app feedback for customers.

- Outcome: Safer driving incentives, improved retention, and better loss ratio on UBI cohorts.

Implementation Roadmap- From Pilot to Scale

A practical roadmap of insurers:

- Find 2-3 high ROI pilots (e.g., triage automation, fraud scoring).

- Form cross-functional teams (product, data, IT, legal).

- Establish data foundations: master data, identity resolution, and a feature store.

- Beta test with definite success criteria.

- Operationise: MLOps, pipelines monitoring, retraining pipelines.

- Scale: cross business line share and standardise platforms.

This is to avoid some of the pitfalls where pilots may do well but fail to take off.

Conclusion

The insurance of the present day is made of data. Insurance data analytics allows the selection of risks with more accuracy, quicker settlement of claims, better customer experience, and the capacity to develop absolutely new products. Although the difficulties of data governance, model explainability, and integration with legacy systems are still there, the possible payback, better loss ratios, reduced operational expenses, and new sources of revenues are too high to justify not investing.

To the insurers who are willing to go beyond proofs-of-concept, the direction is easy to find: identify and develop measurable use cases, develop strong data underpinnings, impose model management, and create value quickly. Data analytics in insurance industry can be a strategic differentiator when approached correctly, converting raw data into wiser insurance for both the customers and sustainable development for the carriers.

FAQs

Data analytics increase the accuracy of underwriting because it uses various data types, including, but not limited to, historical claims, lifestyle data, telematics, and credit to predict the individual risk more accurately. This enables insurers to make quicker, more equitable, and more factual underwriting choices and reduce human prejudice.

Predictive models and AI-driven algorithms are part of data analytics to detect abnormalities and suspicious trends in claims data. The study of claim frequency, policyholder behavior, and network relationships would help the insurers identify possible fraud at an earlier stage and minimise financial losses.

These include auto insurance backed by telematics, which rewards safe drivers, machine vision to determine the extent of vehicle damage, predicting churn models to retain a customer, and weather-related risk forecasting on agricultural or property insurance. These applications present the real-world effects of analytics on profitability and efficiency.

Smaller insurers can begin with the deployment of cloud-based analytics, targeting the high-impact uses such as fraud detection or claims automation. Collaboration with analytics suppliers and insurtech companies will aid in resource limitation and will deploy faster.

The issue of data privacy is paramount, with insurers working with the personal and financial data of a sensitive nature. In order to meet the regulatory requirements, such as GDPR and domestic data protection legislation, insurers need to make sure that when utilizing analytics, they collect data on a consent basis, anonymise it, and implement strong cybersecurity measures.

By

By June 10, 2026

June 10, 2026